The Senior's Guide to Financial Advisors in New Jersey

Struggling with financial confusion and stress? Working with a financial advisor in New Jersey might solve that. Finding the right one can take your personal finance game to the next level.

No matter what stage of life you’re in, getting expert advice takes some of the weight off your shoulders.

Financial planning is crucial, especially for seniors who want to achieve peace of mind in their later years.

Think of it like building a house - you need to have a solid foundation through savings and investments to ensure stability.

Just as home construction takes time and effort, financial planning is also an ongoing process. It’s necessary to review your financial plan and assess if it’s still aligned with your needs and goals.

And working with an expert will make things a lot easier.

You may think you don’t need to hire one right now, but don’t pass up the opportunity to build a better financial future.

This is where a good financial advisor in NJ comes in. They offer expert guidance in all things financial, from managing day-to-day finances to creating a personalized plan.

Take the first step by exploring your options. Leonard Financial Solutions is here to help you make informed decisions as you navigate the complex world of finances.

Key Takeaways

- Understand the role and importance of financial advisors.

- Seniors can work with financial planners and advisors in managing their finances and planning retirement.

- Explore different financial planning services to help you achieve your financial goals.

- Find expert advice for personal financial planning in New Jersey.

What is a Financial Advisor?

Financial advisors aim to help you manage your money, set financial goals, and plan for the future. They provide advice on financial topics like savings, investment strategies, insurance planning, and retirement plans.

Like how you hire an architect or engineer to create a blueprint for your house - a financial advisor helps map out a plan for your financial success.

The Role of a Financial Advisor

A financial advisor helps you make smart financial decisions. They assist with retirement planning, investment strategy, and managing your financial aspects. As part of the financial planning process, an advisor will:

- Meet with the client to discuss and assess financial goals, needs, and overall financial situations.

- Collect information on the client’s income and expenses, retirement plans, and investments like mutual funds. This may include insurance review, asset allocation, risk management, and more.

- Once they’ve gathered enough information, the financial advisor creates a financial plan and recommendations.

Let’s say you want to retire. Your New Jersey financial advisor will guide you on how much to save and where to invest.

For building retirement nest eggs, 401(k) plans or IRAs are common strategies. Whichever account you choose, the goal of your advisor is to create a long-term plan for financial security.

Some advisors follow a fiduciary duty, meaning they must legally act in your best interests. Working with a fiduciary builds trust because you know they’re looking out for you. Not all fiduciaries are fee-only, but many are. A fee-only financial advisor is not making a commission from selling financial products.

Regulations Governing NJ Financial Advisors

How Financial Advisors Help Seniors

A financial advisor offers a wide range of services to help their clients manage their finances. Services provided by advisors in NJ include asset allocation and wealth management solutions. We’ll explore each of these categories below.

In New Jersey, financial advisors must follow strict rules. They register with the state or the Securities and Exchange Commission (SEC), depending on their assets under management. The Financial Industry Regulatory Authority (FINRA) plays a part in federal regulation guidelines.

These regulations help protect you from fraud and unfair practices. For example, they ensure transparency about advisor fees. Financial advisors must provide clear information about their fee structure. As clients, you should know whether they're paid by the hour, a flat fee, or through commissions.

Before working with an advisor, it's wise to check their background on the FINRA website to verify whether they are licensed and have a clean record.

However, keep in mind not all financial professionals are required to register with FINRA.

Some advisors, such as those who are registered with the SEC or state regulators, or those who primarily sell insurance products, may not appear on FINRA's database. For a complete background check, you may also need to consult the SEC's Investment Adviser Public Disclosure (IAPD) system and your state's insurance department.

Asset and Wealth Management Services

A large portion of asset and wealth management deals with portfolio management and tax planning. These financial services focus on optimizing financial growth and security.

Strategic portfolio management offers a framework for maximizing returns while minimizing risks. On the other hand, tax planning strategies are designed to reduce tax liabilities and maximize your money’s potential.

Let's look at two key financial services: portfolio management and tax planning and how these can go hand-in-hand.

Portfolio Management and Investment Management Services

Imagine you invest in tech stocks. If the tech sector experiences a downturn, your entire portfolio suffers. Diversifying into other sectors like healthcare or consumer goods can help mitigate this risk.

To preserve and grow your wealth, you need smart portfolio management. This involves creating a mix of investments like stocks, mutual funds, bonds, and real estate.

A financial advisor in NJ can help you choose the right assets based on your goals and risk tolerance.

Example: Diversified Portfolio

- Stocks: Your advisor might divide a percentage of the portfolio into tech companies or healthcare firms.

- Bonds: To diversify your portfolio, it's recommended you get bonds from the government and corporations.

- Real Estate: Lastly, investing in rental properties and Real Estate Investment Trust (REITs) offers steady cash flow and higher yields.

We all know that you shouldn’t put all of your eggs in one basket. It’s a must to spread your investments across different sectors. If the stock market falls, your bonds might still perform well, balancing out the loss.

As your partner in all things financial matters, your advisor can also adjust your portfolio depending on your situation. If you're close to retirement, they may recommend shifting to more conservative investments for lower risks.

Tax Planning and Management

Effective tax planning allows you to make the most of tax deductions and credits, allowing you to invest more. A financial advisor is experienced in developing strategies to manage your tax liabilities. This includes understanding tax breaks and how different investments are taxed.

Example: Tax-Advantaged Accounts

- 401(k) and IRA: Save for retirement and reduce taxable income for the year.

- 529 Plans: Save for education with tax credits for contributions.

- Roth Accounts: Save post-tax dollars for retirement.

An advisor might also help you with strategies like tax-loss harvesting.

According to Investopedia, tax-loss harvesting involves selling investments at a loss to offset gains. This lowers the federal tax owed that year.

To ensure tax efficiency, your financial advisor will review your tax situation and help you with investment planning. This way, you can manage your wealth better.

Retirement Planning Strategies

When you’re planning for retirement, you need to manage your savings and prepare for what happens afterward. The key elements involve effective use of 401(k) and IRA accounts and careful estate planning.

Managing your 401(k) and IRA accounts is essential for securing a better financial future.

401(k) plans allow you to save pre-tax dollars, which can grow tax-deferred until you withdraw them. A financial advisor can help you understand how tax-deferred accounts reduce your taxable income.

Aside from 401(k) plans, IRAs are great retirement investments. A Traditional IRA gives you a tax deduction now, while a Roth IRA lets your money grow tax-free.

Imagine you earn a steady income and seek to maximize retirement savings. By contributing to your employer’s 401(k) and a Roth IRA, you balance immediate tax benefits with future tax-free withdrawals.

A financial advisor in NJ can help you maximize the use of these tax-advantaged accounts. Additionally, they can assist with risk management to ensure your retirement plan is robust and secure.

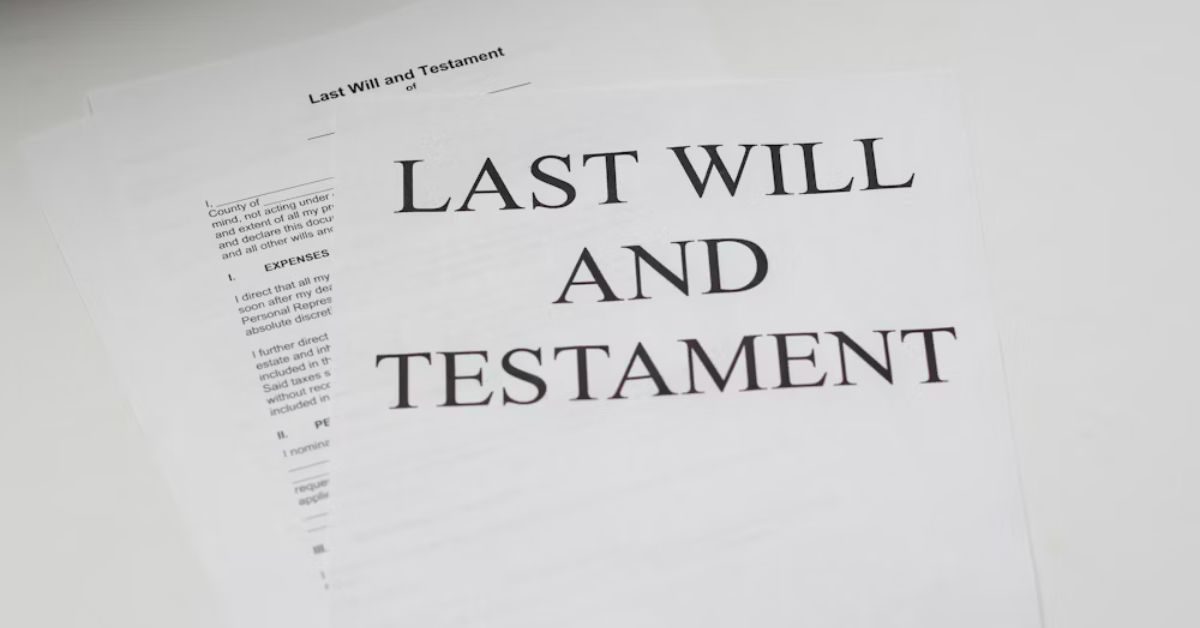

Estate and Succession Planning

Estate management is an important aspect of financial planning for seniors. This ensures your assets are distributed as you wish after your passing.

The most common estate planning strategies are drafting a will and setting up trusts. A will specifies who inherits your assets. Meanwhile, trusts can provide more control over how and when your assets are distributed.

Your financial advisor’s role also includes creating a healthcare directive and power of attorney. This way, your medical and financial wishes are followed if you become unable to make decisions. Naming beneficiaries on your retirement accounts to avoid probate will make it quicker for your heirs to receive funds.

For example, Jane, a 60-year-old business owner in New Jersey, worked with a financial advisor to set up a trust for her grandchildren. This trust ensures her assets are managed and distributed according to her wishes, even after she passes away.

Additionally, Jane updated her will and healthcare directives to reflect her current circumstances, providing her family with clear guidance and peace of mind.

With the help of a financial advisor, it’s easier to go through the complexities of estate management, reassuring you that your family’s well-being is in good hands.

How To Choose a Financial Advisor in NJ

Working with the right financial advisor helps you avoid the cost of financial illiteracy. A survey by the National Financial Educators Council found that the average American loses over $1,500 due to a lack of financial knowledge.

This is why it’s important to have a financial expert on your side to avoid such situations.

If you're considering a financial advisor in NJ, follow these tips to help you make an informed choice:

Assess Your Financial Needs

Not everyone has the same needs and goals when it comes to finances. Before selecting a financial advisor, consider your financial goals.

For example, do you want to get general or personal financial advice? Do you need help with retirement planning, budgeting, or investments?

Knowing your needs helps to find an advisor who specializes in those areas.

To define your financial needs, examine your short-term and long-term goals.

Short-term financial objectives include paying off credit card debt and building an emergency fund, while long-term goals are related to retirement planning.

You should also consider the stage of your life. Adults who are approaching senior age should focus on maximizing retirement savings and creating a more sustainable income stream.

For personalized advice, you might want to book a free financial planning consultation.

This can give you a clearer understanding of your unique situation and what is required to meet your goals.

Know the Different Types of Advisors

The term “financial advisor” is broad, so make sure you understand the different types of advisors.

Consider whether you prefer a fee-only advisor, who charges for services and has no incentive to sell products, or fee based advisors, who may also earn commissions. A fiduciary is required by law to act in your best interest, which minimizes conflicts of interest.

Understanding their differences will allow you to choose the type that fits your unique needs.

Frequently Asked Questions

Can I do financial planning on my own?

Yes, you can do financial planning on your own, but getting help from a financial planner offers a lot of benefits. They provide industry know-how, experience, and an objective perspective to develop a financial plan.

What do financial advisors do for their clients?

Financial advisors typically help their clients with tax planning, investment management, asset allocation, and more.

You may set in person meetings with a potential advisor to identify which service suits your needs.

What are the qualifications to look for in a top financial advisor in New Jersey?

You should check for qualifications like a Certified Financial Planner (CFP) designation. Look for years of experience, education, and other certifications like Chartered Financial Analyst (CFA).

While these certifications establish financial advisors’ credibility, earning certifications is not mandatory.

How can I find reviews for credible financial advisors in NJ?

You can find reviews on websites like Yelp, Google Reviews, or specialized financial advisor directories like BrokerCheck by FINRA. Asking friends or family for recommendations can also help.

What should I expect to pay for fee only financial advisors in NJ?

Fee structure typically depends per advisor. Fee only financial advisors may charge an hourly rate between $150 and $400, or fixed client fees ranging from $1,000 to $5,000 every year. Some may also have a percentage-of-assets fee ranging from 0.5% to 1.5%.

What are the benefits of working with a registered investment advisor in New Jersey?

Registered investment advisors are fiduciaries, meaning they must legally act in your best interests. They provide personalized advice and typically offer a wider range of investment options compared to brokers.

Is it worth it to have a financial advisor?

The short answer is yes. Advisors in NJ provide valuable expertise, guidance, and personalized strategies to help you reach your goals, manage risk, and plan for the future. Your peace of mind may justify the cost of hiring a financial planner.

Which is better financial advisor or planner?

The terms financial advisors and financial planners are often used interchangeably.

In general, financial advisor is considered broader because they refer professionals who offer debt management, investment strategy, business planning, personalized wealth management, and more.

Meanwhile, a financial planner looks at the entire financial picture and long-term goals. It depends on your overall objectives when it comes to your finances.

At what point in terms of savings or investment should I consider consulting a financial advisor?

Consider consulting a financial advisor if you have $50,000 or more in savings or investments. It's also smart to get advice when you’re planning for retirement, buying a home, or saving for college.

Check their Credentials and Qualifications

If you want to find a trustworthy and qualified professional, doing your due diligence is key.

You can verify an advisor’s registration status through reputable sources like FINRA and SEC. These organizations usually maintain databases where you can research advisors’ backgrounds, disciplinary history, and other relevant information.

What Should You Look for in NJ Financial Advisors?

When choosing a financial advisor in New Jersey, there are some criteria to consider. These credentials and qualifications can help ensure you get reliable financial advice.

Certifications and Degrees

Financial advisors in NJ may have certifications and professional designation. Some examples are CFA (Chartered Financial Analyst) and CFP (Certified Financial Planners).

The CFP certification is recognized for its rigorous education and ethical standards. To become a CFP, advisors complete coursework on financial topics, pass an exam, and gain relevant experience.

Meanwhile, the CFA designation focuses on investment management and financial analysis. It requires passing a series of exams, considered some of the toughest in the financial industry.

Besides certifications, financial advisors usually have degrees in finance, economics, or business. Many have a Bachelor's or Master's degree. This educational background ensures they understand complex financial concepts and can apply them effectively.

Experience and Specializations

As much as possible, look for advisors with several years of experience managing client finances.

Experienced advisors have dealt with different financial situations, which helps them provide better advice. Moreover, they are equipped with industry knowledge and expertise.

Some advisors specialize in areas like retirement planning, tax strategies, or estate planning. If you need specific financial services, finding an advisor with experience in that area can provide tailored advice to your needs.

Client Testimonials

When it comes to building credibility, nothing beats genuine reviews and testimonials from real people. When deciding on a financial advisor in NJ, consider their overall reputation.

Client testimonials offer direct insight into the experiences of others. Reading these can help you gauge not just the satisfaction of past clients but also the advisor's reliability.

Look for testimonials that praise the advisor's transparency and dedication. Make sure the testimonials mention consistent communication and personalized advice. Genuine reviews often highlight these qualities because they foster trust.

Always be cautious of reviews that are overly positive without details, as they might be less credible.

Another tip is to type “financial advisors near me” or “top rated financial advisors” on search engines like Google. Through this approach, you explore Google reviews of potential advisors and gain insights into others’ experiences.

Current Trends in New Jersey's Financial Advisory Scene

ESG Investing

One notable trend is the focus on Environmental, social, and governance (ESG) investing. This refers to the practice of investing “sustainably.”

Financial advisors in NJ recommend investing in companies. These companies focus on social and environmental responsibility. ESG investing reflects investors' desire to align their portfolios with their values.

The industry is also adapting to changes in market dynamics.

With economic changes, advisors stay updated with the latest trends to better guide you through uncertain times. This proactive approach helps in managing your financial goals better.

Innovation

In innovation, there's a rise in the use of data analytics. Advisors use data-driven strategies to predict market trends and make informed decisions. By leveraging this technology, they can offer more accurate and effective advice.

Holistic Approach to Financial Solutions

Emphasis on education is also a key trend.

Advisors are spending more time educating clients. They teach about financial planning, investing, and market changes. By focusing on comprehensive financial planning, seniors can make better-informed financial decisions.

Schedule a Free Consultation on Financial Planning

Scheduling a free consultation is the first step to addressing your financial goals. Whether you're planning for retirement, managing debt, or looking to invest, discussing your needs with a skilled advisor can make a big difference.

Why Schedule a Consultation?

A consultation allows you to:

- Assess your financial health

- Set realistic goals

- Create a personalized plan

This consultation is crucial for understanding your current financial situation and planning for the future.

Meet Jonathan Leonard

Jonathan Leonard, an independent fiduciary, serves all New Jersey residents. He has years of experience helping clients navigate their financial journeys. Primarily working with retirees, Jonathan can help you make informed retirement decisions.

How to Schedule

Booking a free financial planning consultation with Jonathan is easy. Simply visit theappointment page to get started. You can select a time that fits your schedule and look forward to a productive discussion.

What to Expect

- Initial Assessment: Jonathan will review your financial information.

- Goal Setting: Identify short-term and long-term goals.

- Personalized Plan: Receive a tailored plan and financial services suited to your needs.

Feel free to bring any questions or concerns. This is your time to get guidance and clarity.

Benefits of a Free Consultation

- No Cost: No obligation or cost for the first meeting.

- Expert Advice: Benefit from Jonathan’s expertise.

- Personal Attention: Focused, personalized advice for your situation.

Begin your journey toward financial confidence today. Schedule your free consultation and take control of your overall financial life.

Get a No-Cost Consulation

At Leonard Financial Solutions, we're committed to making your financial planning straightforward and stress-free.

Contact Us today to see how we can help you save time and money while securing a safe retirement.

LEONARD FINANCIAL SOLUTIONS

Start Planning Your Secure Retirement Today

We are dedicated to helping you achieve a safe and secure retirement. Whether you're in New Jersey, or anywhere in the United States, our independent fiduciary team is here to provide expert guidance tailored to your needs.